Climatic Volume X- Climate volume detection

- Relative volume value in bar

- Automatic zone generation (possibility of configuration)

- Additional features

¡¡¡Thumbs up¡¡¡

חפש סקריפטים עבור "relative volume"

Parabolic Move Indicator for catching moves with Penny Stocks.

Catch the day’s first big moves! Track premarket gap-ups or gap-downs, then spot early momentum shifts using volume, RSI, VWAP, EMAs, and breakout levels—perfect for acting on strong intraday setups right at market open.

**Description:**

The Parabolic Move Scanner + VWAP Bands + EMAs indicator helps traders identify **high-probability intraday moves**, particularly immediately after market open. It is ideal for stocks that **gap up or down premarket, pull back slightly, and then show renewed strength or weakness** once regular trading begins.

The indicator combines multiple components for precise signals:

* **Relative Volume Filter: ** Highlights bars with unusually high activity to ensure signals are backed by real participation.

* **RSI Momentum Change: ** Detects sudden momentum shifts to identify early strength or weakness.

* **Recent Highs/Lows Breakout: ** Confirms price is breaking short-term resistance or support.

* **VWAP & Standard Deviation Bands: ** Provides intraday trend reference points, with optional daily reset.

* **Exponential Moving Averages (EMAs): ** Tracks trend across short, medium, and long-term intraday periods.

* **Visual Signals: ** Background highlights and horizontal breakout lines make it easy to spot key bars.

* **Alerts: ** Configurable alerts notify you of bullish or bearish parabolic moves.

**Optimal Use Case: **

Use in the first 15–30 minutes after market open at 1 minute Time Frame. Best for **stocks showing a premarket gap followed by a pullback**, then resuming strength (bullish) or weakness (bearish). The combination of **volume, RSI, breakouts, VWAP, and EMAs** ensures you identify the **day’s biggest marktet open moves especially with penny stocks moves** with higher confidence.

---

### **Recommended Settings**

**Component** | **Recommended Setting** | **Description / Purpose**

| **Volume Average Length** | 20 bars | Period for calculating average volume to detect relative spikes. |

| **Volume Multiplier** | 2.0 | Current bar volume must exceed 2× average to signal high activity. |

| **RSI Length** | 7 bars | Short-term RSI period to measure momentum changes. |

| **RSI Change Threshold** | 7 | Minimum RSI change required to trigger momentum signal. |

| **Recent Highs Lookback** | 5 bars | Number of bars to check for short-term breakout levels. |

| **Horizontal Line Length** | 10 bars | Length of horizontal breakout line drawn on the chart. |

| **Horizontal Line Color** | Green (bullish) / Red (bearish) | Visual identification of breakout levels. |

| **Horizontal Line Thickness** | 1 | Line width for breakout visualization. |

| **VWAP Source** | hlc3 | Price source for VWAP calculation. |

| **VWAP Bands Multipliers** | 1×, 2×, 3× | Standard deviation multiples for intraday bands.

| **VWAP Daily Reset** | Enabled | Resets VWAP at the start of each trading day.

| **EMA Lengths** | 9, 13, 20, 33, 50 | Short, medium, and long-term EMAs to track intraday trend. |

| **Enable Bearish Signals** | True | Allows detection of bearish parabolic moves. |

|

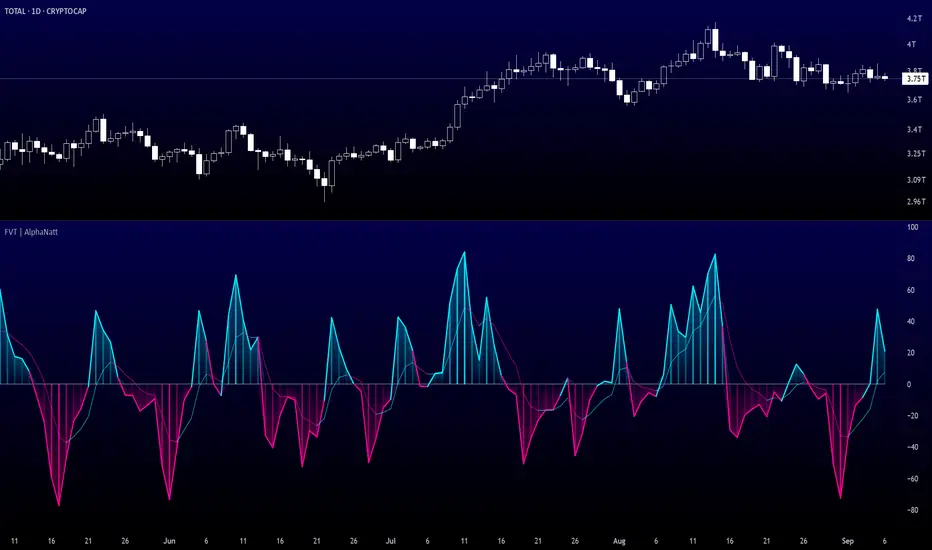

Fisher Volume Transform | AlphaNattFisher Volume Transform | AlphaNatt

A powerful oscillator that applies the Fisher Transform - converting price into a Gaussian normal distribution - while incorporating volume weighting to identify high-probability reversal points with institutional participation.

"The Fisher Transform reveals what statistics professors have known for decades: when you transform market data into a normal distribution, turning points become crystal clear."

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🎲 THE MATHEMATICS

Fisher Transform Formula:

The Fisher Transform converts any bounded dataset into a Gaussian distribution:

y = 0.5 × ln((1 + x) / (1 - x))

Where x is normalized price (-1 to 1 range)

Why This Matters:

Market extremes become statistically identifiable

Turning points are amplified and clarified

Removes the skew from price distributions

Creates nearly instantaneous signals at reversals

Volume Integration:

Unlike standard Fisher Transform, this version weights price by relative volume:

High volume moves get more weight

Low volume moves get filtered out

Identifies institutional participation

Reduces false signals from retail chop

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

💎 KEY ADVANTAGES

Statistical Edge: Transforms price into normal distribution where extremes are mathematically defined

Volume Confirmation: Only signals with volume support

Early Reversal Detection: Fisher Transform amplifies turning points

Clean Signals: Gaussian distribution reduces noise

No Lag: Mathematical transformation, not averaging

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚙️ SETTINGS OPTIMIZATION

Fisher Period (5-30):

5-9: Very sensitive, many signals

10: Default - balanced sensitivity

15-20: Moderate smoothing

25-30: Major reversals only

Volume Weight (0.1-1.0):

0.1-0.3: Minimal volume influence

0.5-0.7: Balanced price/volume

0.7: Default - strong volume weight

0.8-1.0: Volume dominant

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📊 TRADING SIGNALS

Primary Signals:

Zero Cross Up: Bullish momentum shift

Zero Cross Down: Bearish momentum shift

Signal Line Cross: Early reversal warning

Extreme Readings (±75): Potential reversal zones

Visual Interpretation:

Cyan zones: Bullish momentum

Magenta zones: Bearish momentum

Gradient intensity: Strength of move

Histogram: Raw momentum power

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🎯 OPTIMAL USAGE

Best Market Conditions:

Range-bound markets (reversals clear)

High volume periods

Major support/resistance levels

Divergence hunting

Trading Strategies:

1. Extreme Reversal:

Enter when oscillator exceeds ±75 and reverses

2. Zero Line Momentum:

Trade crosses of zero line with volume confirmation

3. Signal Line Strategy:

Early entry on signal line crosses

4. Divergence Trading:

Price makes new high/low but Fisher doesn't

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Developed by AlphaNatt | Quantitative Trading Systems

Version: 1.0

Classification: Statistical Transform Oscillator

Not financial advice. Always DYOR.

Volume Auto FitThis does nothing more than decreasing the size of (absolute) volume candles a bit, in order to allow showing candles with "Absolute" volume and Relative volume inside of the same panel - to save space.

I want to see both because:

Relative volume indicates higher activity than usual

Absolute volume helps with "Volume Price Analysis"

On the 5m you don't need "Volume Auto fit", but can just use usual "Volume" and it will look fine.

For the 1D I've created this one though, since RVol can be gigantic there sometimes.

FlowFusion Money Flow — FP + VWAP Drift + PVT (−100..+100)Title (ASCII only)

FlowFusion Money Flow — Flow Pressure + Rolling VWAP Drift + PVT (Normalized −100..+100)

Short Description

Original money-flow oscillator combining Flow Pressure, Rolling VWAP Drift, and PVT Momentum into one normalized score (−100..+100) with a signal line, thresholds, optional component plots, and ready-made alerts.

Full Description (meets “originality & usefulness”)

What’s original

FlowFusion Money Flow is not a generic mashup. It builds a single score from three complementary, volume-aware components that target different facets of order flow:

Flow Pressure (FP) — In-bar directional drive scaled by relative volume.

Drive

=

close

−

open

max

(

high

−

low

,

tick

)

∈

=

max(high−low, tick)

close−open

∈ .

Relative Volume

=

volume

average volume over

𝑓

𝑝

𝐿

𝑒

𝑛

=

average volume over fpLen

volume

.

𝐹

𝑃

𝑟

𝑎

𝑤

=

Drive

×

RelVol

FP

raw

=Drive×RelVol then squashed (softsign) to

.

Why it belongs: distinguishes real pushes (big body and big volume) from noise.

Rolling VWAP Drift — Direction of VWAP itself over a rolling window, normalized by ATR.

𝑉

𝑊

𝐴

𝑃

𝑡

=

∑

(

𝑇

𝑃

×

𝑉

𝑜

𝑙

)

∑

𝑉

𝑜

𝑙

VWAP

t

=

∑Vol

∑(TP×Vol)

over vwapLen.

Drift

=

𝑉

𝑊

𝐴

𝑃

𝑡

−

𝑉

𝑊

𝐴

𝑃

𝑡

−

1

𝐴

𝑇

𝑅

=

ATR

VWAP

t

−VWAP

t−1

→ squashed to

.

Why it belongs: persistent VWAP movement signals sustained accumulation/distribution.

PVT Momentum — Price-Volume Trend standardized (z-score) and squashed.

𝑃

𝑉

𝑇

𝑡

=

𝑃

𝑉

𝑇

𝑡

−

1

+

𝑉

𝑜

𝑙

×

Δ

𝐶

𝑙

𝑜

𝑠

𝑒

𝐶

𝑙

𝑜

𝑠

𝑒

𝑡

−

1

PVT

t

=PVT

t−1

+Vol×

Close

t−1

ΔClose

.

𝑧

=

𝑃

𝑉

𝑇

−

SMA

(

𝑃

𝑉

𝑇

)

StDev

(

𝑃

𝑉

𝑇

)

z=

StDev(PVT)

PVT−SMA(PVT)

→ squashed to

.

Why it belongs: captures volume-weighted trend pressure without relying on price alone.

Composite score:

Score

=

𝑤

𝐹

𝑃

⋅

𝐹

𝑃

+

𝑤

𝑉

𝑊

𝐴

𝑃

⋅

𝑉

𝑊

𝐴

𝑃

_

𝐷

𝑟

𝑖

𝑓

𝑡

+

𝑤

𝑃

𝑉

𝑇

⋅

𝑃

𝑉

𝑇

_

𝑀

𝑜

𝑚

𝑤

𝐹

𝑃

+

𝑤

𝑉

𝑊

𝐴

𝑃

+

𝑤

𝑃

𝑉

𝑇

Score=

w

FP

+w

VWAP

+w

PVT

w

FP

⋅FP+w

VWAP

⋅VWAP_Drift+w

PVT

⋅PVT_Mom

with a Signal = SMA(Score, sigLen). Thresholds mark strong accumulation/distribution zones.

How it works (step-by-step)

Compute FP, VWAP Drift, PVT Momentum.

Normalize each to the same

scale.

Weighted average → FlowFusion Score.

Smooth with a Signal line to reduce whipsaw.

Optional background shading when Score exceeds thresholds.

How to use

Direction filter:

Score > 0 favors longs; Score < 0 favors shorts.

Momentum turns:

Score crosses above Signal → setup for long; below → setup for short.

Strength zones:

Above Upper Threshold (default +40) = strong buy pressure; below Lower (−40) = strong sell pressure.

Confluence:

Best near S/R, trendlines, or HTF bias. For scalping on 1–5m, consider sigLen 9–13 and thresholds ±40 to ±50.

Alerts included: zero cross, zone entries, and Score/Signal crossovers.

Inputs (key)

fpLen (20): relative-volume lookback for Flow Pressure.

vwapLen (34): rolling VWAP window.

pvtLen (50): PVT z-score window.

sigLen (9): Signal smoothing.

Weights: wFP, wVWAP, wPVT to bias the blend.

Thresholds: upperBand / lowerBand (defaults +40/−40).

Display: toggle component plots and background shading.

Best practices

Trending markets: increase wVWAP (VWAP Drift) or widen thresholds.

Ranging markets: increase wFP and wPVT; take quicker profits.

News: wait for bar close confirmation or reduce size.

Data quality: use consistent volume feeds (especially in crypto).

Limitations

Oscillators can stay extreme in strong trends; use structure/trend filters.

Volume anomalies (illiquid pairs, API glitches) can distort signals—sanity-check with another venue when possible.

Disclaimer

This indicator is for educational purposes only and is not financial advice. Trading involves risk; past performance does not guarantee future results. Always paper-trade first and use appropriate risk controls.

Ludvig Indicator PROThe Ludvig Indicator is designed to identify high-probability breakout setups by combining trend, volume, volatility, and relative strength filters. It helps you enter stocks (or ETFs/crypto) when institutional money is likely flowing in, while avoiding false breakouts and weak trends.

🔑 Core Features

Zero-Lag EMA (ZLEMA)

Faster, less lagging trend detection compared to traditional EMAs.

Used as the basis for dynamic ATR bands.

ATR Volatility Bands

Adaptive bands based on the Average True Range (ATR).

Define the zone where price must close outside to confirm trend strength.

Breakout Confirmation

Requires price to close above recent highs (lookback configurable).

Ensures signals are “true breakouts,” not just noise around moving averages.

Volume Filter (Relative Volume)

Validates breakouts with significantly higher volume than average.

Prevents low-liquidity signals from triggering.

Trend Strength (ADX)

Built-in ADX calculation ensures only strong, trending moves are considered.

Default filter: ADX ≥ 18 (configurable).

Relative Strength vs. Benchmark

Compares the asset’s momentum against a benchmark (default: SPY).

Only signals when the asset is outperforming the benchmark.

Useful for sector rotation and picking leaders instead of laggards.

Alerts & Signals

Breakout entries are marked with small green triangles.

Built-in alerts for automated notifications (TradingView alerts).

VSA - The Volume HUDVSA Volume HUD: Your At-a-Glance Volume Dashboard

Tired of cluttered charts with multiple indicators taking up screen space?

The VSA Volume HUD is a clean, powerful, and fully customisable Heads-Up Display that puts all the critical volume and price action data you need into one compact box, right on your chart.

Designed for traders who rely on Volume Spread Analysis (VSA), this tool helps you instantly gauge the strength, conviction, and context behind every price move as it happens.

Key Features

This indicator isn't just about showing the current volume; it provides a comprehensive, real-time analysis of the market's activity.

Real-time VSA Dashboard: A persistent on-screen table that updates with every tick, giving you instant feedback without needing to look away from the price. The HUD is fully draggable (hold Ctrl/Cmd + click and drag) to place it anywhere you like.

Essential Volume Metrics:

Current Volume: Displayed in a clean, abbreviated format (e.g., 1.25M for millions, 54.3K for thousands).

% Change (vs. Previous Bar): Instantly see if volume is expanding or contracting.

Vs Short-Term Average: Compare the current bar's volume to a moving average to spot unusual spikes.

Volume Velocity: Measures the rate of change in volume over a short period, helping you spot acceleration or deceleration in market interest.

Relative Volume (RVOL): See how the current volume compares to the average for that specific time of day, perfect for identifying abnormally high or low activity.

Price Action & Volatility Context:

Range vs. ATR: Quickly determine if the current bar's volatility is expanding or contracting compared to the recent average.

Price vs. VWAP: See how far the current price has deviated from the session's Volume-Weighted Average Price, a key level for institutional traders.

Deep Customization is Key

Tailor the HUD to perfectly match your trading style and chart aesthetic.

Display & Layout:

Compact Mode: Remove the metric labels for a sleek, minimalist view that saves screen space.

Bar Meters: Enable optional visual bars next to key metrics for a quick, graphical representation of strength.

Total Control: Toggle every single metric on or off to build the exact dashboard you need. Adjust text size, position, and background opacity with ease.

Smart Coloring & Visual Alerts:

Advanced VSA Coloring: This isn't just about up/down candles. The script intelligently colors volume based on confluence. It highlights increasing volume on a strong up-bar (bullish confirmation) or increasing volume on a down-bar (potential climax or distribution), giving you a deeper VSA context.

High Volume Highlight: Make standout bars impossible to miss! The entire HUD background can change color automatically when volume surges past a custom threshold (e.g., over 150% of the average), instantly drawing your attention to critical moments.

Full Color Customization: Change every color to match your chart's theme, including separate colors for bullish/bearish moves, the background, and the border.

How to Use It

The VSA Volume HUD is a powerful confirmation tool. Use it to:

Confirm Breakouts: Look for a spike in Volume vs. Average and RVOL as price breaks a key level.

Spot Exhaustion: Notice high volume on a narrow-range candle after a long trend, visible through the Range/ATR metric.

Gauge Conviction: Use the Advanced Coloring to see if volume is supporting the price move (e.g., green volume on a green candle) or diverging from it.

Impulse Volume Oscillator [Alpha Extract]Impulse Volume Oscillator

A sophisticated indicator designed to identify market impulse moves and volume-based momentum shifts, helping traders capture significant price movements with precision.

Combining price deviations with volume analysis, this oscillator dynamically measures market strength and weakness, providing clear signals for potential trend continuations and reversals.

🔶 Volume-Adjusted Normalization

Utilizes a unique normalization technique that incorporates volume impact to enhance signal quality. This approach ensures the indicator responds more strongly to high-volume price movements while filtering out low-volume noise.

vol_ratio = ta.rsi(volume, 14) / 50

vol_factor = vol_impact > 0 ? 1 + (vol_ratio - 1) * vol_impact : 1

raw_normalized = dev / (ta.stdev(source, bars) * mult)

vol_adjusted = raw_normalized * vol_factor

normalized = ta.sma(vol_adjusted, smooth)

🔶 Adaptive Regime Detection

Incorporates threshold-based regime identification that clearly distinguishes between trending and mean-reverting market conditions. The customizable threshold system allows traders to adapt to different market volatilities and timeframes.

🔶 Customizable Parameters

Fine-tune detection sensitivity with adjustable inputs for lookback period, standard deviation multiplier, volume impact, and signal smoothing. These parameters enable traders to optimize the indicator for various trading styles and market conditions.

❓How It Works

🔶 Impulse Calculation

The oscillator measures price deviation from a moving average baseline, normalized by standard deviation, and then adjusts the signal based on relative volume strength. This creates a responsive yet stable indicator that accurately reflects market momentum.

// Calculate the basis using the selected MA

basis = get_ma(source, bars)

// Calculate the normalized value with volume impact

dev = source - basis

🔶 Dynamic Visualization

The histogram changes color based on signal strength, providing instant visual cues about market conditions. Green bars indicate positive momentum while red bars represent negative momentum, with color intensity reflecting signal strength.

🔶 Trend Confirmation

Built-in trend direction analysis provides confluence with the primary signal, helping traders distinguish between counter-trend bounces and genuine trend reversals. This dual-confirmation approach significantly reduces false signals.

🔶 Visual Alerts & Boundary Tracking

Monitors signal extremes and dynamically adjusts visualization transparency based on signal strength. The indicator highlights particularly strong impulse moves with background shading, making potential trading opportunities immediately apparent.

🔶 Custom Candle Coloring

Optional candle coloring applies the same color logic as the histogram directly to price candles, providing a unified visual framework that helps traders correlate indicator signals with price action.

🔶 Momentum Shift Detection

Automatically identifies important zero-line crossovers that often signify the beginning of new impulse moves. These transition points frequently offer favorable risk/reward entry opportunities.

🔶 Snapshot samples

1 Week

1 Day

15 Min

🔶 Why Choose AE - Impulse Volume Oscillator?

This indicator provides a comprehensive approach to identifying significant market moves by combining volume analysis with price momentum. By offering clear visual signals for both trend continuation and reversal scenarios, it empowers traders to make more informed decisions across various market conditions and timeframes.

Smarter Money Concepts - OBs [PhenLabs]📊 Smarter Money Concepts - OBs

Version: PineScript™ v6

📌 Description

Smarter Money Concepts - OBs (Order Blocks) is an advanced technical analysis tool designed to identify and visualize institutional order zones on your charts. Order blocks represent significant areas of liquidity where smart money has entered positions before major moves. By tracking these zones, traders can anticipate potential reversals, continuations, and key reaction points in price action.

This indicator incorporates volume filtering technology to identify only the most significant order blocks, eliminating low-quality signals and focusing on areas where institutional participation is likely present. The combination of price structure analysis and volume confirmation provides traders with high-probability zones that may attract future price action for tests, rejections, or breakouts.

🚀 Points of Innovation

Volume-Filtered Block Detection : Identifies only order blocks formed with significant volume, focusing on areas with institutional participation

Advanced Break of Structure Logic : Uses sophisticated price action analysis to detect legitimate market structure breaks preceding order blocks

Dynamic Block Management : Intelligently tracks, extends, and removes order blocks based on price interaction and time-based expiration

Structure Recognition System : Employs technical analysis algorithms to find significant swing points for accurate order block identification

Dual Directional Tracking : Simultaneously monitors both bullish and bearish order blocks for comprehensive market structure analysis

🔧 Core Components

Order Block Detection : Identifies institutional entry zones by analyzing price action before significant breaks of structure, capturing where smart money has likely positioned before moves.

Volume Filtering Algorithm : Calculates relative volume compared to a moving average to qualify only order blocks formed with significant market participation, eliminating noise.

Structure Break Recognition : Uses price action analysis to detect legitimate breaks of market structure, ensuring order blocks are identified only at significant market turning points.

Dynamic Block Management : Continuously monitors price interaction with existing blocks, extending, maintaining, or removing them based on current market behavior.

🔥 Key Features

Volume-Based Filtering : Filter out insignificant blocks by requiring a minimum volume threshold, focusing only on zones with likely institutional activity

Visual Block Highlighting : Color-coded boxes clearly mark bullish and bearish order blocks with customizable appearance

Flexible Mitigation Options : Choose between “Wick” or “Close” methods for determining when a block has been tested or mitigated

Scan Range Adjustment : Customize how far back the indicator looks for structure points to adapt to different market conditions and timeframes

Break Source Selection : Configure which price component (close, open, high, low) is used to determine structure breaks for precise block identification

🎨 Visualization

Bullish Order Blocks : Blue-colored rectangles highlighting zones where bullish institutional orders were likely placed before upward moves, representing potential support areas.

Bearish Order Blocks : Red-colored rectangles highlighting zones where bearish institutional orders were likely placed before downward moves, representing potential resistance areas.

Block Extension : Order blocks extend to the right of the chart, providing clear visualization of these significant zones as price continues to develop.

📖 Usage Guidelines

Order Block Settings

Scan Range : Default: 25. Defines how many bars the indicator scans to determine significant structure points for order block identification.

Bull Break Price Source : Default: Close. Determines which price component is used to detect bullish breaks of structure.

Bear Break Price Source : Default: Close. Determines which price component is used to detect bearish breaks of structure.

Visual Settings

Bullish Blocks Color : Default: Blue with 85% transparency. Controls the appearance of bullish order blocks.

Bearish Blocks Color : Default: Red with 85% transparency. Controls the appearance of bearish order blocks.

General Options

Block Mitigation Method : Default: Wick, Options: Wick, Close. Determines how block mitigation is calculated - “Wick” uses high/low values while “Close” uses close values for more conservative mitigation criteria.

Remove Filled Blocks : Default: Disabled. When enabled, order blocks are removed once they’ve been mitigated by price action.

Volume Filter

Volume Filter Enabled : Default: Enabled. When activated, only shows order blocks formed with significant volume relative to recent average.

Volume SMA Period : Default: 15, Range: 1-50. Number of periods used to calculate the average volume baseline.

Min. Volume Ratio : Default: 1.5, Range: 0.5-10.0. Minimum volume ratio compared to average required to display an order block; higher values filter out more blocks.

✅ Best Use Cases

Identifying high-probability support and resistance zones for trade entries and exits

Finding optimal stop-loss placement behind significant order blocks

Detecting potential reversal areas where price may react after extended moves

Confirming breakout trades when price clears major order blocks

Building a comprehensive market structure map for medium to long-term trading decisions

Pinpointing areas where smart money may have positioned before major market moves

⚠️ Limitations

Most effective on higher timeframes (1H and above) where institutional activity is more clearly defined

Can generate multiple signals in choppy market conditions, requiring additional filtering

Volume filtering relies on accurate volume data, which may be less reliable for some securities

Recent market structure changes may invalidate older order blocks not yet automatically removed

Block identification is based on historical price action and may not predict future behavior with certainty

💡 What Makes This Unique

Volume Intelligence : Unlike basic order block indicators, this script incorporates volume analysis to identify only the most significant institutional zones, focusing on quality over quantity.

Structural Precision : Uses sophisticated break of structure algorithms to identify true market turning points, going beyond simple price pattern recognition.

Dynamic Block Management : Implements automatic block tracking, extension, and cleanup to maintain a clean and relevant chart display without manual intervention.

Institutional Focus : Designed specifically to highlight areas where smart money has likely positioned, helping retail traders align with institutional perspectives rather than retail noise.

🔬 How It Works

1. Structure Identification Process :

The indicator continuously scans price action to identify significant swing points and structure levels within the specified range, establishing a foundation for order block recognition.

2. Break Detection :

When price breaks an established structure level (crossing below a significant low for bearish breaks or above a significant high for bullish breaks), the indicator marks this as a potential zone for order block formation.

3. Volume Qualification :

For each potential order block, the algorithm calculates the relative volume compared to the configured period average. Only blocks formed with volume exceeding the minimum ratio threshold are displayed.

4. Block Creation and Management :

Valid order blocks are created, tracked, and managed as price continues to develop. Blocks extend to the right of the chart until they are either mitigated by price action or expire after the designated timeframe.

5. Continuous Monitoring :

The indicator constantly evaluates price interaction with existing blocks, determining when blocks have been tested, mitigated, or invalidated, and updates the visual representation accordingly.

💡 Note:

Order Blocks represent areas where institutional traders have likely established positions and may defend these zones during future price visits. For optimal results, use this indicator in conjunction with other confluent factors such as key support/resistance levels, trendlines, or additional confirmation indicators. The most reliable signals typically occur on higher timeframes where institutional activity is most prominent. Start with the default settings and adjust parameters gradually to match your specific trading instrument and style.

Psych Level ScreenerThis Script is intended for Pine Screener and is not designed as a indicator!!!

Pine Screener is something TradingView has recently added and is still only a Beta version.

Pine Screener itself is currently only available to members that are Premium and above.

What it does:

This screener will actively look for tickers that are close to Pysch level in your watchlist.

Psych level here refers to price levels that are round numbers such as 50,100,1000.

Users can specify the offset from a psych level (in %) and scanner will scan for tickers that are within the offset. For example if offset is set at 5% then it will scan for tickers that are within +/-5% of a ticker. (for $100 psych level it will scan for ticker in $95-105 range)

Once scan is completed you will be able to see:

- Current price of ticker

- Closest psych level for that ticker

- % and $ move required for it to hit that psych level

- Ticker's day range and Average range (with % of average range completed for the day)

- Ticker volume and average volume

Setting up:

www.tradingview.com

Above link will help you guide how to setup Pine screener.

Use steps below to guide you the setup for this specific screener:

1. Open Pine Screener (open new tab, select screener the "Pine")

2. At the top, click on "Choose Indicator" and select "Psych Level Screener"

3. At the top again, click "Indicator Psych Level Screener" and select settings.

4. Change setting to your needs. Hit Apply when done.

a)"% offset from Psych Level" will scan for any stocks in your watchlist which are +/- from the offset you chose for any given psych level. Default is 5. (e.g. If offset is 5%, it will scan for stocks that are between $95-$105 vs $100 psych level, $190-$210 for $200 psych level and so on)

b) ATR length is number of previous trading days you want to include in your calculation. Moving Average Type is calculation method.

c) Rvol length is number of previous trading days you want to include in your calculation.

5. On top left, click "Price within specified offset of Psych. Level" and select true. Then select "Scan" which is located at the top next to "Indicator Psych Level Screener". This will filter out all the stock that meets the condition.

6. At the end of the column on the right there is a "+" symbol. From there you can add/remove columns. 30min/1hr/4hr/1D Trend are disabled by default so if this is needed please enable them.

7. You can change the order of ticker by ascending and descending order of each column label if needed. Just click on the arrow that comes up when you move the cursor to any of the column items.

8. You can specify advanced filter settings based on the variables in the column. (e.g., set price range of stock to filter out further) To do so, click on the column variable name in interest, located above the screener table (or right below "scan") and select "manual setup".

How to read the column:

Current Price: Shows current price of the ticker when scan was done. Currently Pine Screener does NOT support pre/post-hours data so no PM and AH price.

Psych Level: Psych level the current price is near to.

% to Psych Level: Price movement in % necessary to get to the Psych level.

$ to Psych Level: Price movement in $ necessary to get to the Psych level.

DTR: Daily True Range of the stock. i.e. High - Low of the ticker on the day.

ATR: Average True Range of stock in the last x days, where x is a value selected in the setting. (See step 3 in Previous section)

DTR vs ATR: Amount of DTR a ticker has done in % with respect to ATR. (e.g., 90% means DTR is 90% of ATR)

Vol.: Volume of a ticker for the day. Currently Pine Screener does NOT support pre/post-hours data so no PM and AH volume.

Avg. Vol: Average volume of a ticker in the last x days, where x is a value selected in the setting. (See step 3 in Previous section)

Rvol: Relative volume in percentage, measured by the ratio of day's volume and average volume.

30min/1hr/4hr/1D Trend: Trend status to see if the chart is Bullish or Bearish on each of the time frame. Bullishness or Bearishness is defined by the price being over or under the 34/50 cloud on each of the time frame. Output of 1 is Bullish, -1 is Bearish. 0 means price is sitting inside the 34/50 cloud. Currently Pine Screener does NOT support pre/post-hours data so 34/50 cloud is based on regular trading hours data ONLY.

Some things user should be aware of:

- Pine Screener itself is currently only available to TradingView members with Premium Subscription and above. (I can't to anything about this as this is NOT set by me, I have no control) For more info: www.tradingview.com

- The Pine Screener itself is a Beta version and this screener can stop working anytime depending on changes made by TradingView themselves. (Again I cannot control this)

- Pine Screener can only run on Watchlists for now. (as of 03/31/2025) You will have to prepare your own watchlists. In a Watchlist no more than 1000 tickers may be added. (This is TradingView rules)

- Psych level included are currently 50 to 1500 in steps of 50. If you need a specific number please let me know. Will add accordingly.

- Unfortunately this screener does not update automatically, so please hit "scan" to get latest screener result.

- I cannot add 10min trend to the column as Pine Screener does NOT support 10min timeframe as of now. (03/31/2025)

- This code is only meant for Pine Screener. I do NOT recommend using this as an indicator.

- Currently Pine Screener does NOT support pre/post-hours data. So data such as Price, Volume and EMA values are based on market hours data ONLY! (If I'm wrong about this please correct me / let me know and will make look into and make changes to the code)

Other useful links about Pine Screener:

Quick overview of the Screener’s functionality: www.tradingview.com

what do you need to know before you start working? : www.tradingview.com

These links will go over the setting up with GIFs so is easier to understand.

-----------------------------------------------------------------------------------------------------------------

If there are other column variables that you think is worth adding please let me know! Will try add it to the screener!

If you have any questions let me know as well, will reply soon as I can!

Have a good trading day and hope it helps!

Bollinger Bands MTF & Kalman Filter | Flux Charts📈 Multi-Timeframe Kalman Filtered Bollinger Bands Indicator

Introducing our MTF Kalman Filtered Bollinger Bands – a powerful multi-timeframe Bollinger Bands (BB) indicator enhanced with Kalman filtering for superior smoothing and trend analysis. This indicator dynamically adapts Bollinger Bands across multiple timeframes while incorporating volume-based gradient transparency to highlight significant price movements. This indicator is better optimized for lower timeframes.

❓ How to Interpret the Bands & Volume Gradient:

Our indicator combines Lower Timeframe (LTF) and Higher Timeframe (HTF) Bollinger Bands to provide a comprehensive trend analysis. It applies Kalman filtering to the LTF bands, ensuring smoother, noise-reduced signals. The color gradient and relative volume-based transparency offer deeper insights into price strength.

🔹 LTF Bollinger Bands: Shorter-period bands filtered with a Kalman smoothing algorithm, reducing lag and noise.

🔹 HTF Bollinger Bands: Traditional Bollinger Bands plotted on a higher timeframe, offering macro trend analysis.

🔹 Volume Gradient Transparency: The bands adjust their opacity based on relative buy/sell volume, allowing traders to assess momentum strength.

📌 How Does It Work?

1️⃣ Multi-Timeframe Bollinger Bands Calculation

The LTF BB uses Kalman filtering for a smoother price representation, helping to reduce false signals.

The HTF BB is EMA-smoothed for improved trend clarity.

2️⃣ Adaptive Gradient Transparency

The opacity of the fill color between the bands is determined by relative buy/sell volume.

Higher buy volume = stronger bullish signal (greener bands).

Higher sell volume = stronger bearish signal (redder bands).

3️⃣ Dynamic Trend Signals & Breakouts

Buy Signal: When price breaks below the HTF lower band and LTF bands start rising.

Sell Signal: When price breaks above the HTF upper band and LTF bands start falling.

⚙️ Settings & Customization:

🛠 LTF and HTF Bollinger Bands Settings:

Multiplier: The multiplier applied to the BB to determine the upper and lower bands

Length: Define the number of bars determines the BB calculations.

Custom Timeframe Selection: Choose from predefined options (e.g., 5m, 15m, 1H, 4H, etc).

🎨 Gradient & Transparency Settings:

Bullish/Bearish Color Options: Customize colors for uptrend and downtrend conditions.

Max & Min Opacity: Adjust the transparency levels based on volume intensity.

Solid vs. Gradient Mode: Choose between a gradient fill or a solid color mode for clarity.

📌 Recommended Settings for Optimal Use:

1️⃣ Timeframe Selection (LTF -> HTF):

1 min -> 5 min

2 min -> 5 min

3 min -> 15 min

5 min -> 15 min

15 min -> 1 hr

1 hr -> 4 hr

4 hr -> 1 day

2️⃣ Multiplier: Use 2.0 for LTF and 2.25 for HTF

3️⃣Length: Use a length of 20 - 30 bars

🚀 Why Use This Indicator?

✅ Multi-Timeframe Bollinger Bands with Kalman Filtering – Ideal for traders looking for reduced lag and clearer trend signals.

✅ Volume-Based Transparency – See momentum shifts instantly with adaptive opacity.

✅ Dynamic Buy & Sell Signals – Alerts based on price action + volume trends.

✅ Customizable for Any Strategy – Adjust colors, timeframes, and filtering options for personalized trading.

Zanger Volume Ratio (ZVR)Zanger Volume Ratio (ZVR)

Credits:

Most of the underlying code and logic in this script have been adapted from the work originally published by The_Peaceful_Lizard

Overview

The Zanger Volume Ratio (ZVR) is a powerful indicator designed to reveal market dynamics by comparing current cumulative volume to an average determined over a historical look-back period. It uses the concept of relative volume to not only highlight unusual volume spikes, but also uses color to illustrate how today's trading compares to typical levels. This unique method of volume analysis was popularized by Dan Zanger - a trader known for turning $10,775 into $18,000,000 in less than two years - by identifying key shifts in market interest and volume behavior.

Key Features

Volume Pacing Analysis:

The script calculates a volume delta by comparing the cumulative volume at any given moment to an average derived over a user-defined lookback period (Default 20-day). The resulting percentage difference offers a clear visualization and insight into unusual volume activity.

Dynamic Visual Representation:

Choose between either “Columns” or “Area” plot styles to display the percent difference. Additionally, you have the option to switch between a standard plot or a background color display, with customizable transparency, ensuring the indicator fits seamlessly with your chart’s aesthetics.

Dashboard Integration:

A simple dashboard table is displayed on the chart, showcasing the current ZVR value in real-time. With user-configurable position, text size, alignment, and color options, this feature ensures that the key metric is always visible and easy to interpret.

Why Use the Zanger Volume Ratio?

The ZVR is more than just a volume indicator. It acts as a window into market sentiment by highlighting days when trading interest intensifies. Many traders believe that an unusually high volume ratio may confirm trend strength or signal a reversal, making the indicator a valuable tool when used in conjunction with other technical analysis methods.

Whether you’re monitoring stocks, commodities, or forex markets, the Zanger Volume Ratio offers an accessible yet sophisticated method to decode volume dynamics. Its practical design and real-time visual feedback provide traders of all experience levels with critical data to spot high-potential setups.

Chart Description

First Pane: normal Volume Indicator on the foreground, ZVR as Background colors

Second Pane: ZVR Indicator with Column Style (default)

First panel: normal volume indicator in foreground, ZVR as background colors

Second panel: ZVR indicator with column style (default)

Note: This indicator is intended for use on intraday charts only!

Bar composition in 1minute | True candlestick colorThe indicator shows the true color of a bar based on the internal composition on 1 minute timeframe and the final outcome. It uses following parameters of 1minute and current timeframe inputs

relative bar close, average volume vs current volume and finally the volume of internal candles.

It follows following steps:

First, it defines the arrays of high, low, close, volume in one minute timeframe

Second, it identifies the negative and positive volume based on the bar closing at one minute timeframe

Third , it adds all the volume and find whether the overall volume is positive or negative for overall bar in higher timeframe (current timeframe)

Fourth, it compare the volume in current timeframe to average of volume in in current timeframe

Fifth, if relative closing, relative volume (current timeframe) and the combined volume (in 1 minute timeframe) gives same outcome then color of the bar is decided whether the bar is bullish, bearish or inconclusive/contnuation.

Through this you get to check price action in 1minute timeframe and the ultimate outcome in current timeframe. this helps in understanding whether the bar is truly bullish or bearish or continuation of the trend

Feel free to connect for any query.

Equivolume - volume as candle widthDo price action and volume really need to be on separate graphs? Why not display them both on a single graph and reduce the clutter? Presenting Equivolume candles here on TradingView - inspired by the NinjaTrader implementation

This indicator allows you to view traditional OHLC candles but with the additional ability to see relative volume through variations of width and/or transparency

Explanation

- Wide and/or full colour candles have the highest volume

- Thin and/or highly transparent candles have the lowest volume

- The following diagram shows the Equivolume indicator as well as a traditional volume graph along the bottom. You can see that when the volume is highest, the candle is widest and also the most intense color.

- The `Lookback candle count` user parameter specifies the number of candles to use in order to locate the highest volume within that range. All other candle widths in the range will be adjusted relative to this highest volume

Tips

- Toggle off the visibility of the original graph for the instrument to get the best view of the candles when using variable transparency

Gotchas

- Due to a Pine Script limitation a maximum of 500 variable width candles can be drawn on the chart

- If `Lookback candle count` is higher than the total number of available candles for the instrument, then the indicator will fail and not display anything. I’m still investigating how to handle this case better

- Be aware if you are using the `High` setting for the `Transparency range` parameter, candles with the lowest volume will be virtually invisible

Spread AnalyzerThis script plots the relative performance of the viewed security with respect to a selected benchmark. It can be used to identify assets higher than market average potential.

- The plot above is the relative volume.

- The plot below is the relative performance.

Computation is done by applying stochastic to the spread of the asset's current price/obv value to the benchmark defined by the Part1, 2 and 3.

The benchmark can be a portfolio as well:

Part1 = 4*SPY+2*QQQ

Part2 = XAUUSD+EURUSD

-PS: Each part may contain up to 10 symbols.

- The spread is calculated with the following formula

close / (Part1 + Part2 + Part3)

- Color code is based on the stochastic of macd of the spread.

The inputs:

length : lookback length for the stochastic

lenk : Smoothing factor(K) for stochastic

lend : EMA length(D)

MACD Fast / Slow / Smooth : MACD parameters used to determine the color code

Ajau — Volume Spike Split (Buy vs Sell)EN (English Summary)

This indicator highlights volume spikes above average and splits them by candle direction:

Bullish spike (close ≥ open): triangle-up under the bar (+ optional bar coloring)

Bearish spike (close < open): triangle-down above the bar (+ optional bar coloring)

Designed to be single-panel, minimal, and easy on the eyes.

Logic

Average volume = SMA(len)

Threshold modes:

Multiple (x), e.g., 2.0 → current volume > 2× avg

Percent (%), e.g., 100% → equals 2× avg

Spike = volume > threshold

Key Inputs

Use Multiple Instead of % (recommended)

Spike Multiple (x) (default 2.0)

Spike Ratio % (when Multiple is OFF; 100 = 2×)

Volume Average Length (SMA) (default 21)

Color candles on spikes

Show UP/DOWN marker

Quick Start

Add to chart

Set Use Multiple = ON and Spike Multiple = 2.0 for a 2× rule

Turn Color candles on spikes off if you prefer original chart colors

Alerts: Create Alert → Bullish / Bearish Volume Spike

Educational use only. Not financial advice.

แท็กแนะนำ (Tags)

volume spike, relative volume, rvol, high volume, breakout, accumulation, distribution, momentum, volatility, scalping, swing

FSVZO [Alpha Extract]A sophisticated volume-weighted momentum oscillator that combines Fourier smoothing with Volume Zone Oscillator methodology to deliver institutional-grade flow analysis and divergence detection. Utilizing advanced statistical filtering including ADF trend analysis and multi-dimensional volume dynamics, this indicator provides comprehensive market sentiment assessment through volume-price relationships with extreme zone detection and intelligent divergence recognition for high-probability reversal and continuation signals.

🔶 Advanced VZO Calculation Engine

Implements enhanced Volume Zone Oscillator methodology using relative volume analysis combined with smoothed price changes to create momentum-weighted oscillator values. The system applies exponential smoothing to both volume and price components before calculating positive and negative momentum ratios with trend factor integration for market regime awareness.

🔶 Fourier-Based Smoothing Architecture

Features advanced Fourier approximation smoothing using cosine-weighted calculations to reduce noise while preserving signal integrity. The system applies configurable Fourier length parameters with weighted sum normalization for optimal signal clarity across varying market conditions with enhanced responsiveness to genuine trend changes.

// Fourier Smoothing Algorithm

fourier_smooth(src, length) =>

sum = 0

weightSum = 0

for i = 0 to length - 1

weight = cos(2 * π * i / length)

sum += src * weight

weightSum += weight

sum / weightSum

🔶 Intelligent Divergence Detection System

Implements comprehensive divergence analysis using pivot point methodology with configurable lookback periods for both standard and hidden divergence patterns. The system validates divergence conditions through range analysis and provides visual confirmation through plot lines, labels, and color-coded identification for precise timing analysis.

15MIN

4H

12H

🔶 Flow Momentum Analysis Framework

Calculates flow momentum by measuring oscillator deviation from its exponential moving average, providing secondary confirmation of volume flow dynamics. The system creates momentum-based fills and visual indicators that complement the primary oscillator analysis for comprehensive market flow assessment.

🔶 Extreme Zone Detection Engine

Features sophisticated extreme zone identification at ±98 levels with specialized marker system including white X markers for signals occurring in extreme territory and directional triangles for potential reversal points. The system provides clear visual feedback for overbought/oversold conditions with institutional-level threshold accuracy.

🔶 Dynamic Visual Architecture

Provides advanced visualization engine with bullish/bearish color transitions, dynamic fill regions between oscillator and signal lines, and flow momentum overlay with configurable transparency levels. The system includes flip markers aligned to color junction points for precise signal timing with optional bar close confirmation to prevent repainting.

🔶 ADF Trend Filtering Integration

Incorporates Augmented Dickey-Fuller inspired trend filtering using normalized price statistics to enhance signal quality during trending versus ranging market conditions. The system calculates trend factors based on mean deviation and standard deviation analysis for improved oscillator accuracy across market regimes.

🔶 Comprehensive Alert System

Features intelligent multi-tier alert framework covering bullish/bearish flow detection, extreme zone reversals, and divergence confirmations with customizable message templates. The system provides real-time notifications for critical volume flow changes and structural market shifts with exchange and ticker integration.

🔶 Performance Optimization Framework

Utilizes efficient calculation methods with optimized variable management and configurable smoothing parameters to balance signal quality with computational efficiency. The system includes automatic pivot validation and range checking for consistent performance across extended analysis periods with minimal resource usage.

This indicator delivers sophisticated volume-weighted momentum analysis through advanced Fourier smoothing and comprehensive divergence detection capabilities. Unlike traditional volume oscillators that focus solely on volume patterns, the FSVZO integrates volume dynamics with price momentum and statistical trend filtering to provide institutional-grade flow analysis. The system's combination of extreme zone detection, intelligent divergence recognition, and multi-dimensional visual feedback makes it essential for traders seeking systematic approaches to volume-based market analysis across cryptocurrency, forex, and equity markets with clearly defined reversal and continuation signals.

Chartlense Dashboard (Data, Trend & Levels)Chartlense Dashboard (Data, Trend & Levels)

Overview

This dashboard is designed to solve two common problems for traders: chart clutter and the manual drawing of support and resistance levels . It consolidates critical data from multiple indicators into a clean table overlay and automatically plots the most relevant S&R levels based on recent price action. The primary goal is to provide a clear, at-a-glance overview of the market's structure and data.

It offers both a vertical and horizontal layout to fit any trader's workspace.

Key Concepts & Calculations Explained

This indicator is more than a simple collection of values; it synthesizes data to provide unique insights. Here’s a conceptual look at how its core components work:

Automatic Support & Resistance (Pivot-Based):

The dashed support (green) and resistance (red) lines are not manually drawn. They are dynamically calculated based on the most recent confirmed pivot highs and pivot lows . A pivot is a foundational concept in technical analysis that identifies potential turning points in price action.

How it works: A pivot high is a candle whose `high` is higher than a specific number of candles to its left and right (the "Pivot Lookback" is set to 5 by default in the settings). A pivot low is the inverse. By automatically identifying these confirmed structural points, the script visualizes the most relevant levels of potential supply and demand on the chart.

Relative Volume (RVOL):

This value in the table is not the standard volume. It measures the current bar's volume against its recent average (specifically, `current volume / 10-period simple moving average of volume`).

Interpretation: A reading above 2.0 (indicated by green text) suggests that the current volume is more than double the recent average. This technique is used to identify significant volume spikes, which can add conviction to breakouts or signal potential market climaxes.

Consolidated Data for Context:

Other values displayed in the table, such as the EMAs (9, 20, 200) , Bollinger Bands (20, 2) , RSI (14) , MACD (12, 26, 9) , and VWAP (on intraday charts), use their standard industry calculations. They are included to provide a complete contextual picture without needing to load each indicator separately, saving valuable chart space.

How to Use This in Your Trading

This dashboard is designed as a tool for confluence and context , not as a standalone signal generator. Here are some ways to integrate it into your analysis workflow:

As a Trend Filter: Before considering a trade, quickly glance at the EMAs and the MACD values in the table. A price above the key EMAs and a positive MACD can serve as a quick confirmation that you are aligned with the dominant trend.

To Validate Breakouts: When the price is approaching a key Resistance level (red pivot line), watch the RVOL value . A reading above 2.0 on the breakout candle adds significant confirmation that the move is backed by strong interest. The same logic applies to breakdowns below a support level.

To Spot Potential Reversals: Confluence is key. For example, if the price is testing a Support level (green pivot line) AND the RSI in the table is approaching oversold levels (e.g., near 30), it can signal a higher probability reversal setup.

About This Indicator

This indicator was developed by the team at ChartLense to help traders declutter their charts and focus on the data that matters. We believe in making complex analysis more accessible and organized. We hope this free tool is a valuable addition to your trading process.

VSA Signals [odnac]This indicator applies Volume Spread Analysis (VSA) concepts to highlight important supply and demand events directly on the chart. It automatically detects common VSA patterns using price spread, relative volume, and candle structure, with optional trend filtering for higher accuracy.

Features:

Stopping Volume (SV): Signals potential end of a downtrend when heavy buying appears.

Buying Climax (BC): Indicates exhaustion of an uptrend with heavy volume near the top.

No Supply (NS): Weak selling pressure, often a bullish sign in an uptrend.

No Demand (ND): Weak buying interest, often a bearish sign in a downtrend.

Test: Low-volume test bar probing for supply.

Up-thrust (UT): Failed breakout with long upper wick, often a bearish trap.

Shakeout: Bear trap with high-volume wide down bar closing low.

Demand Absorption (DA): Demand absorbing heavy selling pressure.

Supply Absorption (SA): Supply absorbing heavy buying pressure.

Additional Options:

Background highlights for detected signals.

Configurable moving average (SMA, EMA, WMA, VWMA) as a trend filter.

Adjustable multipliers for volume and spread sensitivity.

Legend table for quick reference of signals and meanings.

Alerts available for all signals.

This tool is designed to help traders spot professional accumulation and distribution activity and to improve trade timing by recognizing supply/demand imbalances in the market.

Breakout Volume Momentum [5m]Breakout Volume Momentum Indicator (Pine Script v5)

This TradingView Pine Script v5 indicator plots a green dot below a 5-minute price bar whenever all the breakout and volume conditions are met. It is optimized for live intraday trading (not backtesting) and includes customizable inputs for thresholds and trading session times. Key features and conditions of this indicator:

Gap Up Threshold: Current price is up at least X% (default 20%) from the previous day’s close (uses higher-timeframe daily data) before any signal can trigger.

Relative Volume (RVOL): Current bar’s volume is at least Y× (default 2×) the average volume of the last 20 bars. This ensures unusually high volume is present, indicating strong interest.

Trend Alignment: Price is trading above the VWAP (Volume-Weighted Average Price) and above a fast EMA. In addition, the fast EMA (default 9) is above the slower EMA (default 20) to confirm bullish momentum

tradingview.com

tradingview.com

. These filters ensure the stock is in an intraday uptrend (above the average price and rising EMAs).

Intraday Breakout (optional): Optionally require the price to break above the recent intraday high (default last 30 bars). If enabled, a signal only occurs when the stock exceeds its prior range high, confirming a breakout. This can be toggled on/off in the settings.

Avoid Parabolic Spikes: The script skips any bar with an excessively large range (default >12% from low to high), to avoid triggering on spiky or unsustainable parabolic candles.

Time Window Filter: Signals are restricted to a specific session window (by default 09:30 – 11:00 exchange time, typically the morning session) and will not trigger outside these hours. The session window is adjustable via inputs

stackoverflow.com

.

Alerts: An alert condition is provided so you can set a Trading View alert to send a push notification when a green dot signal fires. The alert message includes the ticker and price at the time of signal.

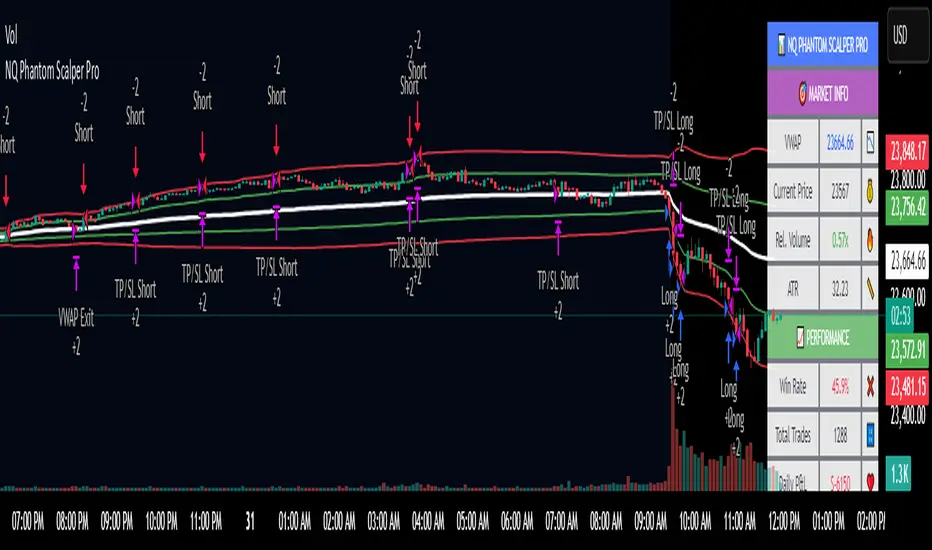

NQ Phantom Scalper Pro# 👻 NQ Phantom Scalper Pro

**Advanced VWAP Mean Reversion Strategy with Volume Confirmation**

## 🎯 Strategy Overview

The NQ Phantom Scalper Pro is a sophisticated mean reversion strategy designed specifically for Nasdaq 100 (NQ) futures scalping. This strategy combines Volume Weighted Average Price (VWAP) bands with intelligent volume spike detection to identify high-probability reversal opportunities during optimal market hours.

## 🔧 Key Features

### VWAP Band System

- **Dynamic VWAP Bands**: Automatically adjusting standard deviation bands based on intraday volatility

- **Multiple Band Levels**: Configurable Band #1 (entry trigger) and Band #2 (profit target reference)

- **Flexible Anchoring**: Choose from Session, Week, Month, Quarter, or Year-based VWAP calculations

### Volume Intelligence

- **Volume Spike Detection**: Only triggers entries when volume exceeds SMA by configurable multiplier

- **Relative Volume Display**: Real-time volume strength indicator in info panel

- **Optional Volume Filter**: Can be disabled for testing alternative setups

### Advanced Time Management

- **12-Hour Format**: User-friendly time inputs (9 AM - 4 PM default)

- **Lunch Filter**: Automatically avoids low-liquidity lunch period (12-2 PM)

- **Visual Time Zones**: Color-coded background for active/inactive periods

- **Market Hours Focus**: Optimized for peak NQ trading sessions

### Smart Risk Management

- **ATR-Based Stops**: Volatility-adjusted stop losses using Average True Range

- **Dual Exit Strategy**: VWAP mean reversion + fixed profit targets

- **Adjustable Risk-Reward**: Configurable target ratio to opposite VWAP band

- **Position Sizing**: Percentage-based equity allocation

### Optional Trend Filter

- **EMA Trend Alignment**: Optional trend filter to avoid counter-trend trades

- **Configurable Period**: Adjustable EMA length for trend determination

- **Toggle Functionality**: Enable/disable based on market conditions

## 📊 How It Works

### Entry Logic

**Long Entries**: Triggered when price touches lower VWAP band + volume spike during active hours

**Short Entries**: Triggered when price touches upper VWAP band + volume spike during active hours

### Exit Strategy

1. **VWAP Mean Reversion**: Early exit when price returns to VWAP center line

2. **Profit Target**: Fixed target based on percentage to opposite VWAP band

3. **Stop Loss**: ATR-based protective stop

### Visual Elements

- **VWAP Center Line**: Blue line showing volume-weighted fair value

- **Green Bands**: Entry trigger levels (Band #1)

- **Red Bands**: Extended levels for target reference (Band #2)

- **Orange EMA**: Trend filter line (when enabled)

- **Background Colors**: Yellow (lunch), Gray (after hours), Clear (active trading)

- **Info Panel**: Real-time metrics display

## ⚙️ Recommended Settings

### Timeframes

- **Primary**: 1-5 minute charts for scalping

- **Validation**: Test on 15-minute for swing applications

### Market Conditions

- **Best Performance**: Ranging/choppy markets with good volume

- **Trend Markets**: Enable trend filter to avoid counter-trend trades

- **High Volatility**: Increase ATR multiplier for stops

### Session Optimization

- **Pre-Market**: Generally avoided (low volume)

- **Morning Session**: 9:30 AM - 12:00 PM (high activity)

- **Lunch Period**: 12:00 PM - 2:00 PM (filtered by default)

- **Afternoon Session**: 2:00 PM - 4:00 PM (good volume)

- **After Hours**: Generally avoided (wide spreads)

## ⚠️ Risk Disclaimer

This strategy is for educational purposes only and does not constitute financial advice. Past performance does not guarantee future results. Trading futures involves substantial risk of loss and is not suitable for all investors. Users should:

- Thoroughly backtest on historical data

- Start with small position sizes

- Understand the risks of leveraged trading

- Consider transaction costs and slippage

- Never risk more than you can afford to lose

## 📈 Performance Tips

1. **Volume Threshold**: Adjust volume multiplier based on average NQ volume patterns

2. **Band Sensitivity**: Modify band multipliers for different volatility regimes

3. **Time Filters**: Customize trading hours based on your timezone and preferences

4. **Trend Alignment**: Use trend filter during strong directional markets

5. **Risk Management**: Always maintain consistent position sizing and risk parameters

**Version**: 6.0 Compatible

**Asset**: Optimized for NASDAQ 100 Futures (NQ)

**Style**: Mean Reversion Scalping

**Frequency**: High-Frequency Trading Ready

A+ Trade CheckList with Comprehensive Relative StrengthThe indicator designed for traders who need real-time market assessment across multiple timeframes and benchmarks. This comprehensive tool combines traditional technical analysis with sophisticated relative strength measurements to provide a complete market picture in one convenient table display.

The indicator tracks essential trading levels including:

QQQ and SPY trend analysis using exponential moving averages

Previous day and week high/low levels for key support and resistance

Market open levels from the first 5 and 15 minutes of trading (9:30 AM ET)

VWAP positioning for institutional price reference

Short-term EMA positioning for momentum assessment

Advanced Relative Strength Analysis

The standout feature of this indicator is its comprehensive 8-metric relative strength scoring system that compares your current ticker against both QQQ (Nasdaq-100) and SPY (S&P 500) benchmarks.

The 4-Metric Relative Strength System Explained

Metric 1: Relative Strength Ratio (RSR)

Purpose: Measures whether your ticker is outperforming or underperforming relative to its historical relationship with the benchmarks.

How it works:

Calculates the ratio of your ticker's price to QQQ/SPY prices

Compares current ratio to a 20-period moving average of the ratio

Scores +1 if ratio is above average (relative strength), -1 if below (relative weakness)

Trading significance: Identifies when a stock is breaking out of its normal correlation pattern with major indices.

Metric 2: Percentage-Based Relative Performance

Purpose: Compares short-term percentage changes to identify immediate relative momentum.

How it works:

Calculates 5-day percentage change for your ticker and benchmarks

Subtracts benchmark performance from ticker performance

Scores +1 if outperforming by >1%, -1 if underperforming by >1%, 0 for neutral

Trading significance: Captures recent momentum shifts and identifies stocks moving independently of market direction.

Metric 3: Beta-Adjusted Relative Strength (Alpha)

Purpose: Measures risk-adjusted performance by accounting for the ticker's natural volatility relationship with benchmarks.

How it works:

Calculates rolling beta (correlation and variance relationship)

Determines expected returns based on benchmark moves and beta

Measures alpha (excess returns above/below expectations)

Scores based on whether alpha is consistently positive or negative

Trading significance: Identifies stocks generating returns beyond what their risk profile would suggest, indicating fundamental strength or weakness.

Metric 4: Volume-Weighted Relative Strength

Purpose: Incorporates volume analysis to validate price-based relative strength signals.

How it works:

Compares VWAP-based percentage changes between ticker and benchmarks

Applies volume weighting factor based on relative volume strength

Enhances score when high relative volume confirms price movements

Trading significance: Distinguishes between genuine institutional-driven moves and low-volume price action that may not sustain.

Combined Scoring System

The indicator generates 8 individual scores (4 metrics × 2 benchmarks) that combine into a single strength assessment:

Score Interpretation

Strong (4-8 points): Ticker significantly outperforming both benchmarks across multiple methodologies

Moderate Strong (1-3 points): Ticker showing good relative strength with some mixed signals

Neutral (0 points): Balanced performance relative to benchmarks

Moderate Weak (-1 to -3 points): Ticker showing relative weakness with some mixed signals

Weak (-4 to -8 points): Ticker significantly underperforming both benchmarks

Display Format

The indicator shows results as: "Strong (6/8)" indicating the ticker scored 6 out of 8 possible points.

Volume CandlesVolume Candles — Context-Aware Candle Color

Description:

This visual indicator colors your price candles based on relative volume intensity, helping traders instantly detect low, medium, and high volume activity at a glance. It supports two modes — Percentile Ranking and Volume Average — offering flexible interpretation of volume pressure across all timeframes.

It uses a 3-tiered color system (bright, medium, dark) with customizable tones for both bullish and bearish candles.

How It Works:

You can choose between two modes for volume classification:

Ranking Mode (Default):

Measures current volume’s percentile rank over a lookback period. Higher percentiles = stronger color intensity.

Percentile thresholds:

< 50% → light color (low volume)

50–80% → medium intensity

> 80% → high volume

Volume Average Mode:

Compares current volume against its simple moving average (SMA).

Volume thresholds:

< 0.5× SMA → light color

Between 0.5× and 1.5× → medium

> 1.5× → high intensity

Candle Paint:

Candles are colored directly on the chart, not in a separate pane. Bullish candles use green shades, bearish use red. All colors are fully customizable.

How to Interpret:

Bright Colors = High volume (potential strength or climax)

Muted/Transparent Colors = Low or average volume (consolidation, traps)

Example Use Cases:

Spot fakeouts with large price movement on weak volume (dark color)

Confirm breakout strength with bright candles

Identify stealth accumulation/distribution

Inputs & Settings:

Mode: Ranking Percentile or Volume Average

Lookback Period for ranking and SMA

Custom Colors for bullish and bearish candles at 3 intensity levels

Best For:

Price action traders wanting context behind each candle

Scalpers and intraday traders needing real-time volume feedback

Anyone using volume as a filter for entries or breakouts

Pro Tips:

Combine with Price Action, Bollinger Bands or VWAP/EMA levels to confirm breakout validity and intent behind a move.

Use alongside RSI/MACD divergences for high-volume reversal signals.

For swing trading, expand the lookback period to better normalize volume over longer trends.